Modular insurance is not new. Most insurance comes with policy options. Examples of modularity include:

For example, the proposition of Universal Life is to provide premium flexibility, while combining transparent savings and protection options.

Customer centricity has grown to become a priority goal in the insurance industry. Insurers are striving to better match their products to the needs of modern customers. They recognize that modularity is a key enabler for providing flexibility and choice to their customers. A breakthrough modular product proposition would create significant competitive advantage.

Modular products have financial advantages too. Insurers aim to shift product portfolios away from guaranteed return products and into protection and investment-linked products for lower capital costs and higher margins. These higher-margin product categories fit naturally within a modular framework and make it easier for customers to recognize their value.

Changing product strategy is often slow due to existing distribution and operations practices. For meaningful change, insurers may need a bold approach. By introducing modularity, existing business practices need to change. That’s always hard, but a better option than selling only legacy low-margin products that customers increasingly view as past their “sell by” dates.

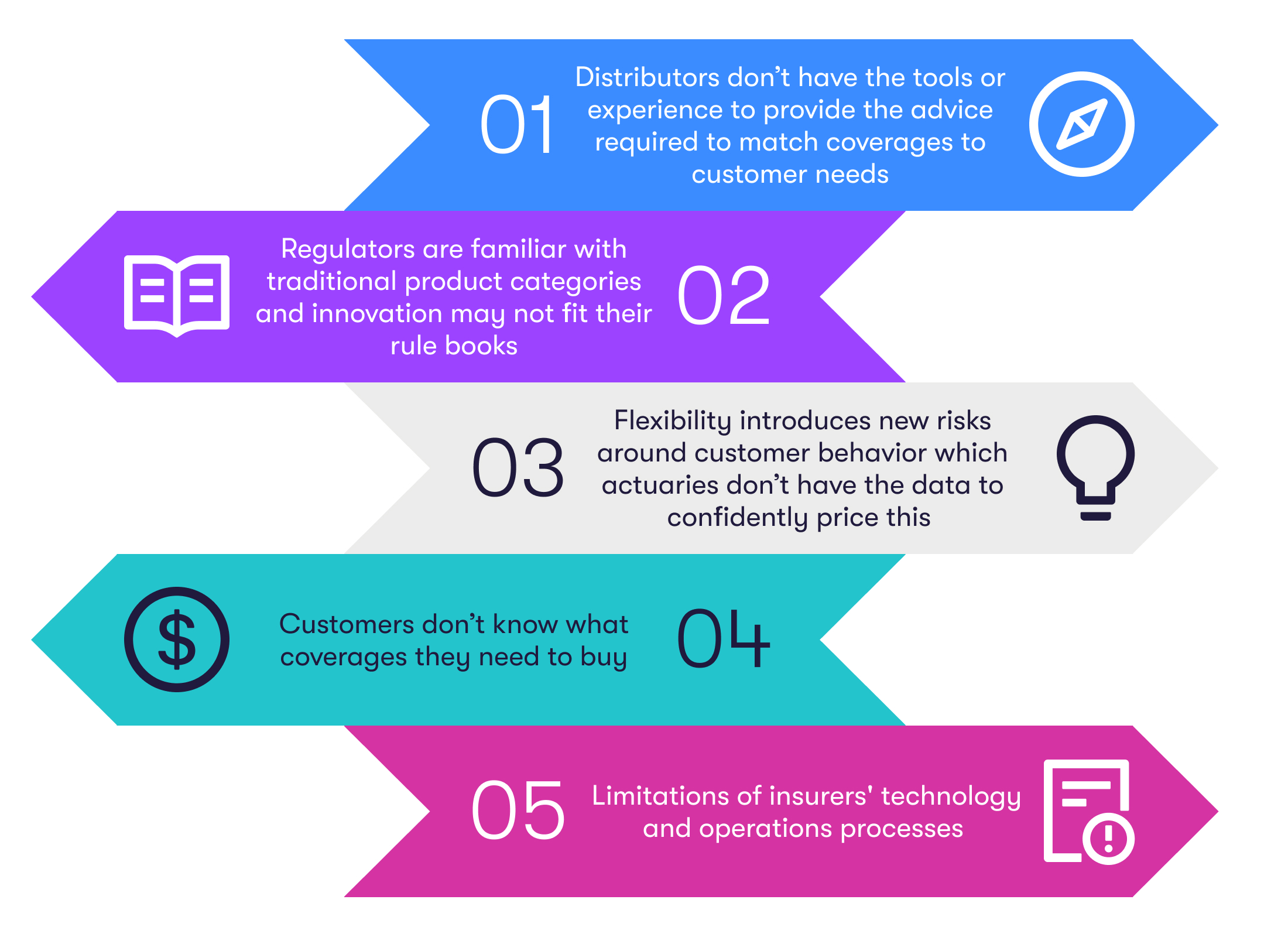

It’s hard to deliver modular products

Despite the industry’s creativity, and insurers aspiring to modularity, we have not yet seen a breakthrough into truly modular products. This is because:

At the point of sale, there are challenges for using existing technology to sell modular products:

-

Recommend modules to customers from a menu:

Existing needs-analysis tools are compliance-driven, confirming that a product the distributor wants to sell is appropriate, rather than making detailed recommendations on coverages that match the customer’s needs. -

Illustrate combinations of modules:

Quotation systems take customer information and deliver the price of a product. This is fine if the customer buys one product, but for multiple modules, the customer would need to obtain multiple quotations – not a good customer experience. Bespoke programming of the quotation system will be needed to illustrate the total cost and benefits of all the possible combinations of modules on offer to customers. -

Pricing combinations of modules:

The actuarial price of an individual module may depend on the other modules that the customer buys in combination with that module. For example, if a customer buys a savings module in combination with a life protection module; this may indicate that the customer takes a positive view of their own heath because they are saving for the future. Providing quotations that depend on other modules requires more than lookups to premium tables.

Coherent Spark as a modular product engine

Coherent Spark deploys models and logical rules from Microsoft Excel to a controlled IT environment. It automatically builds an API for each model to provide ready connectivity into front- and back-end systems.

Life and general insurers use Spark to deploy product recommendation algorithms. These start as simple logical rules for module recommendation based on customer responses to a set of questions. The level of sophistication grows over time, as the “menu” of module options increases and the algorithm has access to richer data– for example, real-time data from a distribution partner to get insights into customer lifestyle choices. Spark’s flexibility enables the insurer to change, UAT test, and deploy the amended logic–all in just a fraction of the time that would be possible with traditional, hard-coded systems.

Product recommendation algorithms deployed by Coherent clients via Spark create robo-advisory tools to support customers in making online purchases from a set of options. Spark is also used by Coherent clients to deploy algorithms in tools that support advisors in face-to-face sales: matching an analysis of customer needs and budget to the right set of product modules.

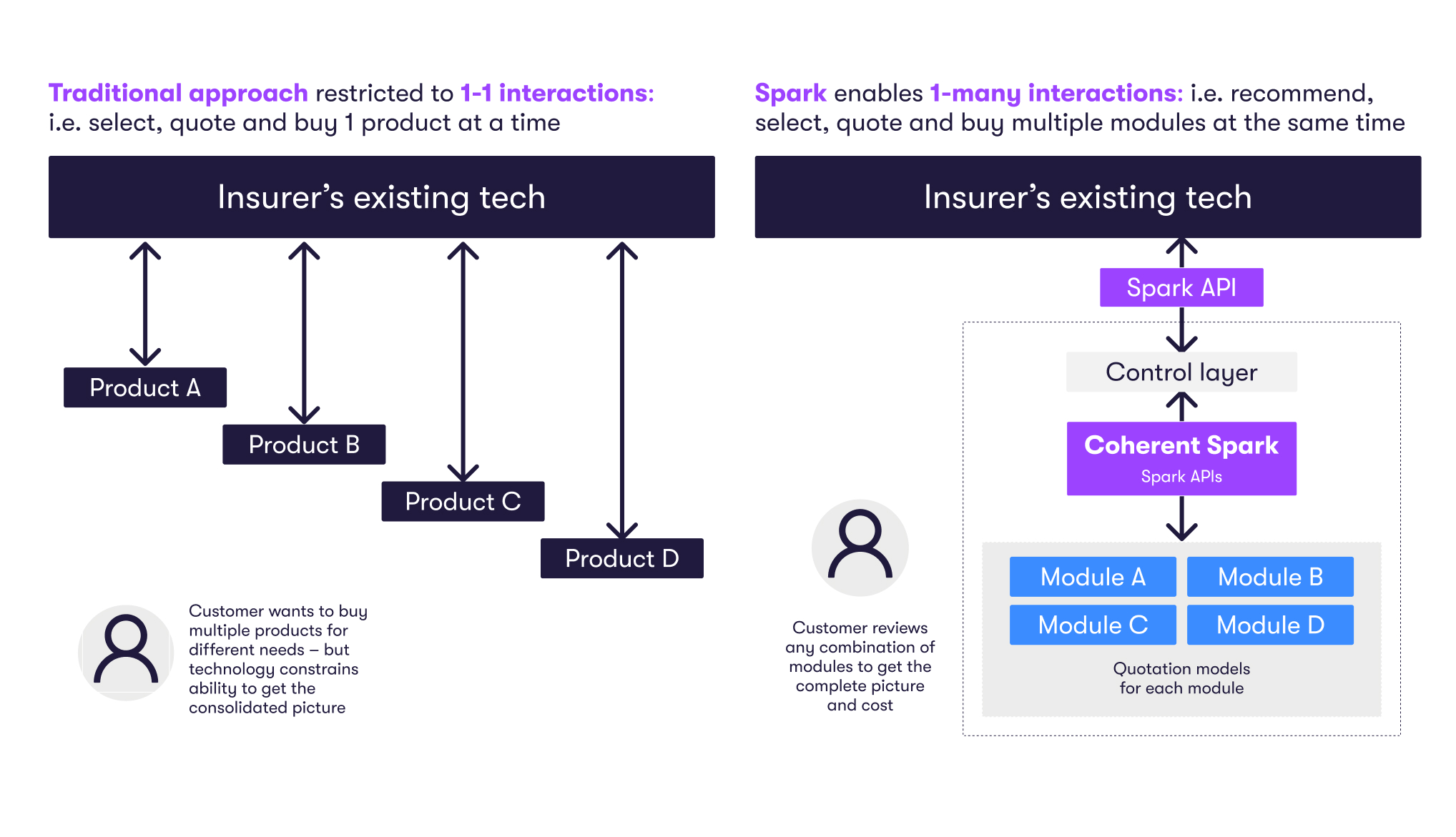

Pricing and illustration of combinations of modules

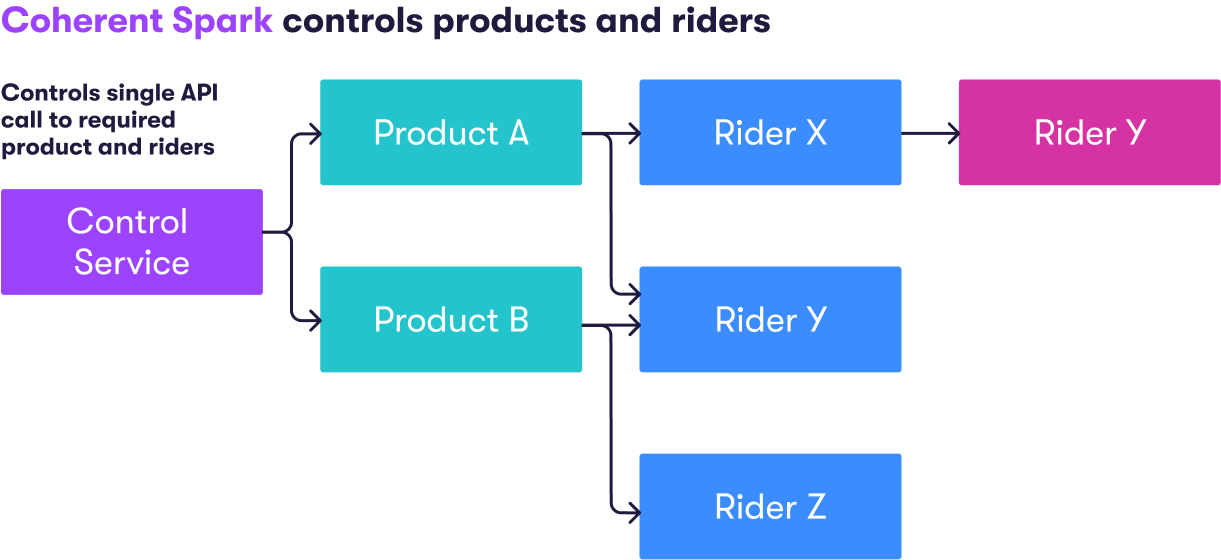

Insurers with modular product strategies require the full power of Spark for pricing combinations of modules selected by each customer. Pricing engines in Spark provide premium quotations for each module separately based on the pricing model for each module. Then a Spark ‘control service’ of combination logical rules takes these individual module quotations to provide the customer with the correct aggregate price for the selected combination of modules.

Spark’s own design is modular, so it is a natural fit for modular products:

For example, if a customer buys Modules A and C then the price may not be the same as the sum of A and C separately. Spark’s control service delivers the required pricing for the A and C combination to the customer and enables a visual illustration in the front-end.

This modularity of Spark means that the product delivery team can readily add, delete, and amend product modules without any hardcoding. For example, if the insurer replaces Module D by Module D1 in the above diagram, then the revised Module D1 pricing slots into the overall quotation system – it is plug-and-play.

Dynamic illustration of modular options

When customers review insurance options, they need to check prices and then iterate to:

- Match the options under consideration to the available budget.

- Experiment with alternative benefits and features to assess which are highest priority to meet their needs: for example, balancing protection against savings within a fixed premium budget.

Every changed input, like moving a slider on a front-end to increase premium allocation to a protection option, makes an API call to Spark and returns the new quotation to the front-end for dynamic, instantaneous presentation.

Agile product development

An insurer with a modular product framework can readily test and learn from the customer response to new modules, new features, and repricing. This requires an agile approach to product development and marketing: with the menu of customer options evolving over time as market needs and the competitive environment changes. Frequent module repricing (in particular, refining the combination pricing highlighted above) is more important than with traditional products, as new data is continuously gathered on customer experience and behaviours in the new modular environment.

Developing new insurance products takes months from proposition development to market launch. Insurers are working hard to speed up the process, but speed-to-launch constraints reinforce a strategy of periodic new ‘blockbuster’ products. Not the agile, iterative, strategy that best fits a modular approach.

Fortunately, Spark supports an agile product development culture. Spark’s no-code capability for deploying new modules, or module repricing, means that the product team can rapidly deploy amended modules without requiring programming and testing.

Modular product case studies

-

Investment Linked product with riders

A major regional insurer’s lead product in a key South East Asian market is an Investment Linked product with minimal intrinsic life cover but supported by a full menu of protection riders. The level of rider attachment is high, which is critical to achieve the target profit margin. The product illustration model for the core product and riders is complex. A single, exceptionally large, master spreadsheet contains all the pricing. The legacy process was to provide this to the IT department for coding up into the quotation system. This was a very lengthy, months long process and required significant testing.

Although the product works well, the development process was not flexible. Adding a new rider, or repricing an existing one, required changes to the master spreadsheet and then recoding and retesting the whole model. The complexity and cost of this process discouraged repricing the riders, even when competitive or actuarial considerations would have made this desirable.

With Coherent Spark, the cumbersome master spreadsheet could be replaced with separate illustration models for the core product and each of the riders separately. A Spark control service manages the combination pricing of the core and selected riders for each customer.

With Spark, changes in any rider requires only the model for that rider to be changed. The product team uploads the new model to Spark instantly, without any need for hardcoding. Only the new module needs to go through UAT. Spark provides a modular framework with plug-and-play flexibility.

-

Embedded insurance for a digital bank

A start-up digital bank had made fast progress in adding younger customers for its deposit, credit card and loan products. The bank had successfully created differentiation versus traditional banks with a modern brand and convenient user experience.

The next phase of the bank’s strategy was to add a wider set of financial products, including insurance. The aim for insurance was to offer coverages relevant to younger customers. Market research showed that these younger customers had a negative view of insurance – regarding it as complex and designed for older generations – and had little or no existing insurance cover.

Coherent worked with the bank to create a menu of coverages focused on health, income protection and property cover relevant to younger people. We created product bundles appropriate for personas typical of digital bank customers: including students, frequent leisure travellers, and young professionals.

The bank deploys a product recommendation algorithm via Spark.The bank’s app offers relevant product bundles to each customer to create a personalised experience. Customers either pick the proposed product bundle or adjust the coverages according to their needs and budget. Spark readily enables dynamic quotations for adjusted cover.

The bank is learning all the time and needs to refresh the menu and bundle selections frequently as they gather new customers and learn what works. The flexibility for frequent repricing is also important as claims experience grows. The product menu is set up in a modular framework within Spark. Changes to any module by the bank simply require uploading a new model (for that module only) to Spark – there is no need to recode and retest the whole the system. Spark enables a highly iterative approach to the evolution of the bank’s insurance proposition.

-

Enabling rookie insurance agents to support customer decisions

An agency focused insurer needed to support rookie agents to become more confident advising their clients on making decisions. The insurer recognised that a comprehensive needs analysis, matching individual needs across its full range of available investment and protection products would be too ambitious. Equally, the insurer wanted all its agents to provide clients with real and useful choices; not to push the latest hot product to all clients regardless of individual needs and preferences.

To make the sales process manageable for rookie agents the insurer selected a limited set of customer options. The feedback from the agents was that the trade-offs most often raised by customers were:

- i. How should I balance protection versus savings within my available budget?

- ii. Should I prioritize life cover? Or also purchase critical illness insurance?

- iii. I prefer guaranteed returns on my savings, but my future return will be extremely low unless I take more risk. How do I balance this?

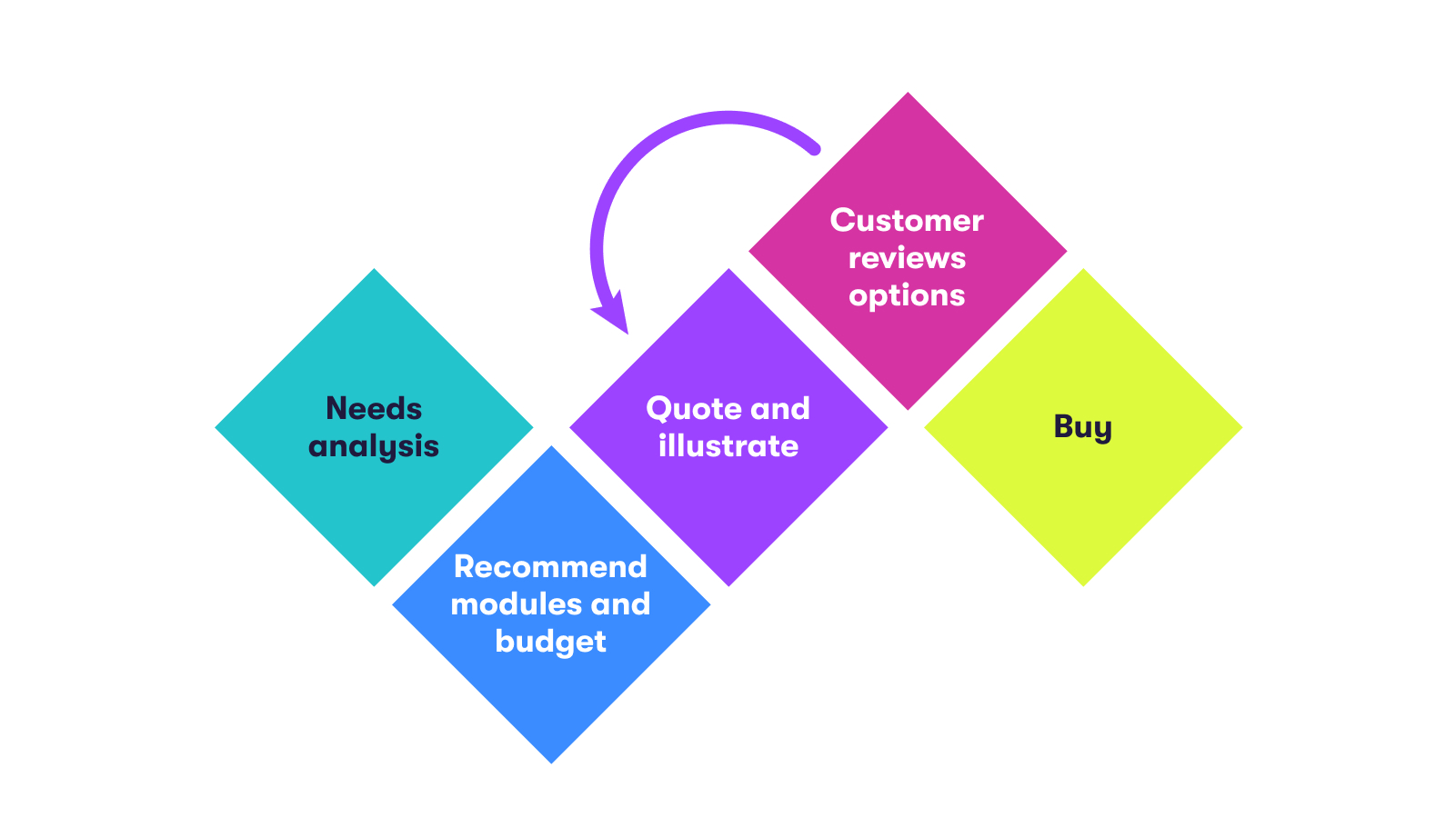

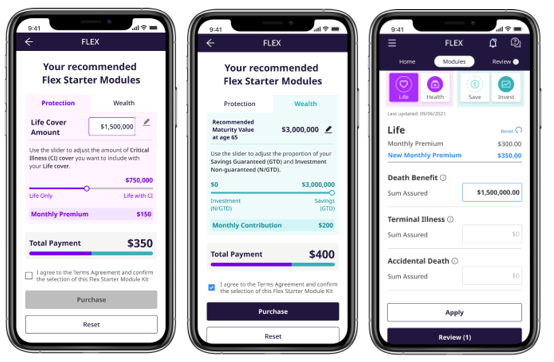

Coherent worked with the insurer to select the key trade-offs for agents to discuss with their clients using a new sales tool. Coherent Spark enables customers to explore these trade-offs dynamically – showing revised costs and benefits instantly as the customer varies the input parameters:

The sales tool facilitates a discussion between agent and customer as follows:

- I. Establish premium budget.

- II. Show customer the projected protection and savings outcomes based on the selected allocation of the available premium budget between protection versus savings. Show how the projections change as the selected inputs change.

- III. Illustrate the impact on the sum assured of adding critical illness cover to life protection within the same premium budget.

- IV. Illustrate how projected returns increase on the customer’s savings, for a given premium, by increasing the allocation of that premium to a non-guaranteed return product.

Spark powers the dynamic quotations to create a useful and engaging discussion between agent and customer. This adds credibility to the rookie agent, as answers to their customer’s ‘what-if’ questions are visually presented to the client in real time.

-

Holistic protection: Life and General Insurance combination

A composite insurer aimed to increase the proportion of customers buying both Life and General Insurance products. The prize was to increase the sale of higher margin life products to the substantial number of General Insurance customers paying smaller premiums. Life and General products are sold by the insurer through different channels: direct-to customer for General Insurance and through an agency channel for Life. Efforts to encourage General customers to contact an agent online had not been successful.

The solution was to provide a holistic online needs analysis that included both Life and General coverage. As the recommendation algorithm became more personalized, the more likely General customers were to consider their wider needs. Deploying the recommendation algorithm via Coherent Spark enabled an iterative approach to building logic that made General customers consider a Life product.

-

A comprehensive modular product strategy

A life insurer aimed to redefine itself in a key market because it was too reliant on a single distribution channel with a limited product range. To grow both business volumes and margins it decided that it needed to adopt a modular product strategy: offering a wider range of options to a wider range of customers.

Ensuring that customers would receive the right advice to select appropriate benefit options was a major challenge. It was also a major opportunity to provide a truly differentiated customer proposition.

The insurer identified the steps required to implement this strategy. It became clear that the insurer would need to embark on a business transformation process. Coherent was engaged to review the role of technology changes required as part of this transformation.

A gap analysis led to a technology roadmap. We found that parts of the insurer’s existing technology could be adapted to support the new strategy. A challenge was the need for a product engine that could deliver the more complex recommendation and quotation logic for a fully modular solution. This required a new “middle layer” between the customer facing systems and policy administration system. Coherent Spark became the agreed option.

Embarking on the modular product journey

Coherent has had dozens of conversations with CEOs, actuaries, and distribution teams across the globe on product strategy. There is a near unanimous view that modular products will ultimately be the norm for the insurance industry. The next industry leaders will be insurers that achieve three key goals:

- An attractive menu of customer options.

- Delivery of the necessary support to customers to help them make the right choices.

- The ability to sell high premium/high margin products as part of the choices available.

Most insurers already have elements of modularity in their products. The journey to a fully modular approach can start small and evolve over time: testing and learning what works towards achieving these three goals.

Embarking on this journey requires:

- Clarity on your product proposition.

- Product design: How many modules should you offer? How could the selected modules fit together as more than the sum of their parts?

- Establish what your customers need: What data do we have? How can you get insights into required coverages and savings goals?

- Bring distribution teams, including for new digital channels, into the product development process. Full modularity requires substantial changes in customer advice. This means a transformed sales process, which your distribution leaders can support because they believe it will lead to competitive advantage.

- Review technology infrastructure and operations processes. What are the gaps? What will need upgrading? What new technology will be needed?

The challenges with modularity are real. Yet the technology is available to overcome them. It is time to take another look at modular products.

To learn more about how Coherent Spark can benefit your company, contact us to schedule a demo and a discussion with our actuarial and technology teams. This white paper has focused on Coherent Spark, our no-code Excel to API capability, as a modular product engine. Modularity also requires highly flexible front and backends. The flexibility of other Coherent solutions (Coherent Sonic for transaction management/Coherent Flow for point-of-sale applications/Coherent Connect for customer outreach) makes them a great fit for new modular propositions.

Bob Charles

Head of Actuarial, Coherent

Bob Charles is an actuary who enjoyed a 30-year career with Willis Towers Watson, culminating in leading the Asia Pacific business. He subsequently worked with insurance technology start-ups. Bob is currently the Head of Actuarial at Coherent, working with clients on finding great uses-cases and applications for our unique Spark technology.