Consumer or Retail Banks across the globe, whether big or small, face common challenges. From New York to Hong Kong, customers are flooded by choices from financial services providers. Today’s banks must continuously evolve to stay ahead of the hyper-competitive curve. On top of this, they are typically behemoths that can be bogged down by their own size and complexity, hindering their ability to quickly change the way they do things. This is further compounded by the fact that “transform the bank” initiatives can come with an astronomical price tag and take years to complete, achieving varying levels of success.

So how should banks transform themselves without “breaking the bank”?

A recent McKinsey report estimates that, on average, a bank’s operations take up 15-20% of its total budget. And digital transformation is usually at the top of senior management’s agenda, typically with two-fold intent: first, to streamline operations and second, to deliver distinctive services and experiences to their customers. As a result, IT backlogs have dramatically ballooned in recent years, as evidenced by a Salesforce survey of IT decision-makers May 2021, in which 88% said their workloads had increased over the last 12 months.

The challenge with software development is that it is slow, complex, and expensive – plus it requires hiring highly technical resources. With No Code Development Platforms (NCDP), leading banks are taking advantage of being able to develop and deploy apps by reducing the pressure on their IT teams and minimizing manual coding as well as maintaining these codes. According to Gartner, 80% of technology products and services will be built by those who are not technology professionals by 2024. With these NCDPs, businesses can automate time-consuming manual coding processes and speed up their delivery. No-code development platforms can reduce technology costs by dispersing some of the “lighter” responsibilities of the specialized and costly IT department.

By 2024, 80% of technology products and services will be built by non-technology professionals -Gartner

How does this work?

In the early days of computer science, instructing a computer to perform tasks required exact placement of vacuum tubes, wires, and punch cards. Everything required writing code – even simple tasks like storing and printing documents. As technology advanced, platforms and apps were put into place that allowed increasingly complex tasks to be completed without coding skills. At the same time, programming languages were becoming increasingly accessible – it’s common for even elementary school students to take coding classes in school. NCDPs represent the convergence of these trends: platforms with the power of traditional coding languages, but without requiring the same level of specialized knowledge.

NCDPs allow users to develop applications through configurations, expressions, and simple statements, often through a user-friendly graphical interface. NCDPs “democratize” coding, so that more people – even non-programmers – can participate and become citizen developers. This reduces the pressure on the IT teams, streamlines IT backlogs, and gives business users and functions more autonomy and freedom to direct the outcome of what they aim to achieve.

An oft-overlooked, but important example of the power of no-code is Microsoft Excel. It began as a way to organize tables and data, but has continued to add increasingly complex features. In fact, it is now considered “Turing-Complete,” which means it can fully replicate the functionality of any other programming language. This has empowered business users to create tools and models right on their desktop without any code.

No-code is just the first component of NCDPs, though. Without a proper development platform providing controls, testing, and integration capability, even traditionally coded applications risk becoming orphaned, fractured, or forgotten. To fully recognize the advantages of no-code development, it is more important than ever to put the right platforms, tools, and processes in place.

Leveraging NCDPs in Banking

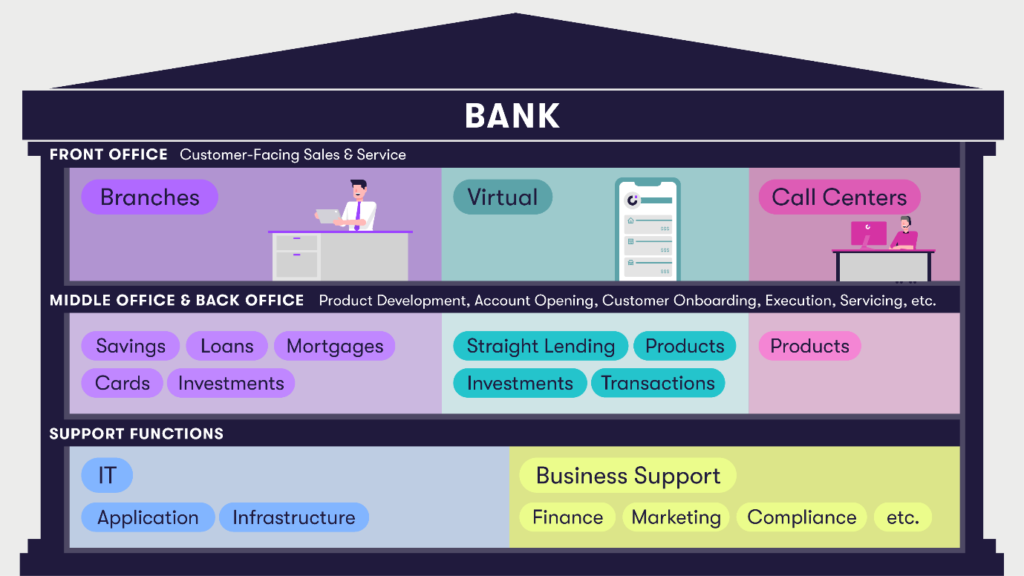

In banking, specifically consumer banking, there is high potential for no-code development platforms to add immediate value across the front, middle and back offices, as well as support functions (See Figure 1).

Figure 1: The Consumer / Retail Bank Operating Model

Banks are complicated, highly regulated enterprises, with complex rules and calculation logic underpinning their operations across all functions, processes, and products. A common misconception is that each of these components requires a distinct IT system to run the bank. However, many functions within most banks still use Excel-based calculations or models to manage, monitor and perform their work.

In the past, common wisdom has been that “modernization” requires migrating these no-code applications into specialized or proprietary systems. Billions of dollars and thousands of hours were spent in what was often the futile pursuit of a suitably modern system. Even when the projects were successful, companies often found themselves saddled with complex, esoteric systems with even higher maintenance costs than the original systems that preceded them.

Leading banks are realizing that the solution isn’t to take control away from their citizen developers. Instead, they empower their employees by providing tools and platforms that allow no-code applications to be part of a robust ecosystem of knowledge assets. This reduces duplication of effort and directs productivity toward value-creating projects.

Adding Value to the Front Office

A recent McKinsey Consumer Banking-focused survey revealed that shopping for new products and account openings are the least satisfying retail-banking customer journeys in today’s post-pandemic era.

Shopping for new products and account openings are the LEAST satisfying of all retail banking customer journeys. -McKinsey Banking Journey Pulse Benchmark 2021

To differentiate themselves from the competition, consumer banks across the globe are finding themselves having to bridge the gap between their existing offerings and changing demands and expectations. Digitally savvy customers expect user-friendly interfaces and consistent experience across multiple platforms and devices. These applications need to then integrate with complex back-end systems that may pre-date mobile phones.

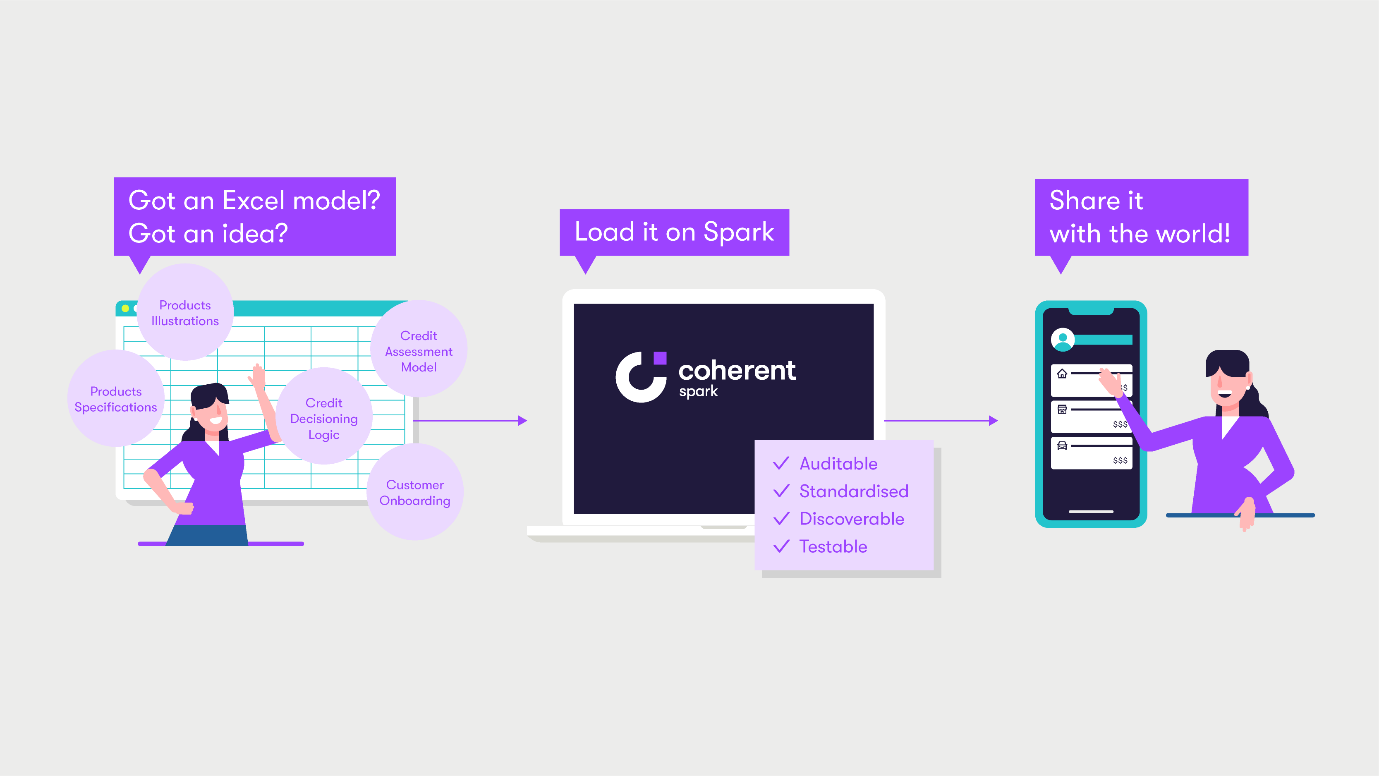

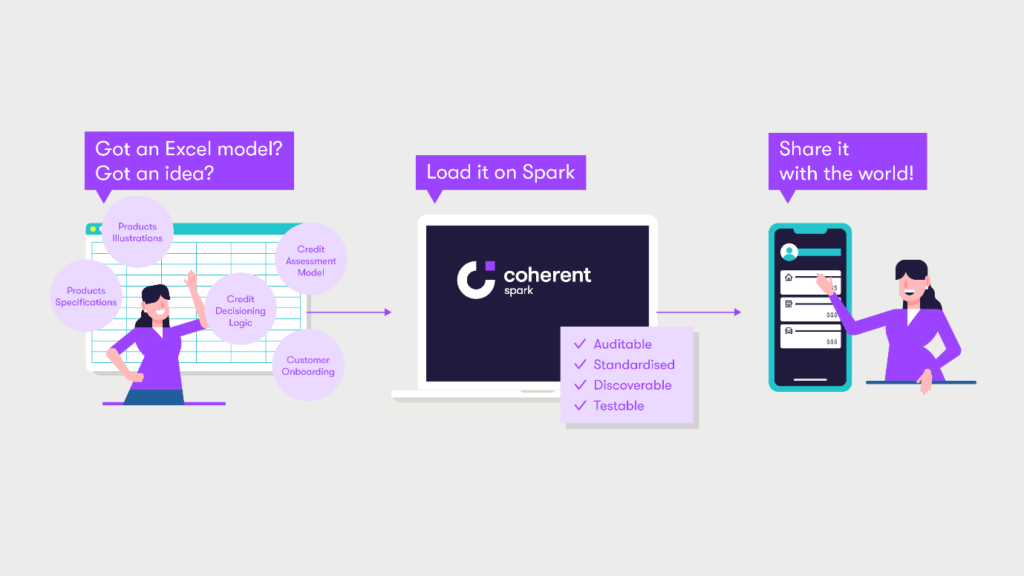

On the sales front, brick and mortar banks have equipped branch personnel with tablets and apps to illustrate scenarios for lending products to prospective customers. Digital and neo-banks help customers choose the best products and services for their needs through web and mobile channels – all self-service and on-demand with only a few clicks. These sales tools reduce the friction encountered when a customer shops for new products and enable smoother customer acquisition and sales processes, which can be applied across different consumer banking products from cards, loans, mortgages, to especially more complex investment and wealth products. As an example, a mortgage Excel model embedded with its various sensitivity analyses can be connected to a front-end user interface to dynamically illustrate the impact of changing interest rates on a specific plan a customer may be considering purchasing.

Proper design and user-experience for these apps is already a challenge, but the product logic is typically too complex to code directly in the front-end. Since the underlying data is stored in the back-end mainframe and core banking systems, the logic and rules are often set up there, but this requires translation into an archaic programming language. Application developers are forced to choose between these two sub-optimal solutions.

NCDP like Coherent Spark can bridge this gap by serving as a middle layer containing the logic and rules. Because these platforms are no-code, subject matter experts can configure the logic directly and avoid the long cycle of writing specifications, testing, and iterating on IT implementation. These product models are often already created in Excel spreadsheets as part of the development process. When combined with the power of a fully API-enabled development platform, this logic is accessible for both front- and back-end systems.

In addition, NCDPs improve and simplify compliance by automating documents and audit trail generation. This is of immense help when banks need to respond to market shifts quickly.

Helping Middle Office & Back Office achieve operational excellence

The account opening process is fraught with frustrating requirements for new customers. And on the flip side, for banks the customer onboarding process is manual and time consuming, with the detailed regulatory requirements imposed globally by various jurisdictions. Despite the digitization wave, this process is still by and large paper-based and consumes a lot of time for both the customer and the financial institution. The daunting prospect of a tiresome process can discourage potential clients from even opening an account.

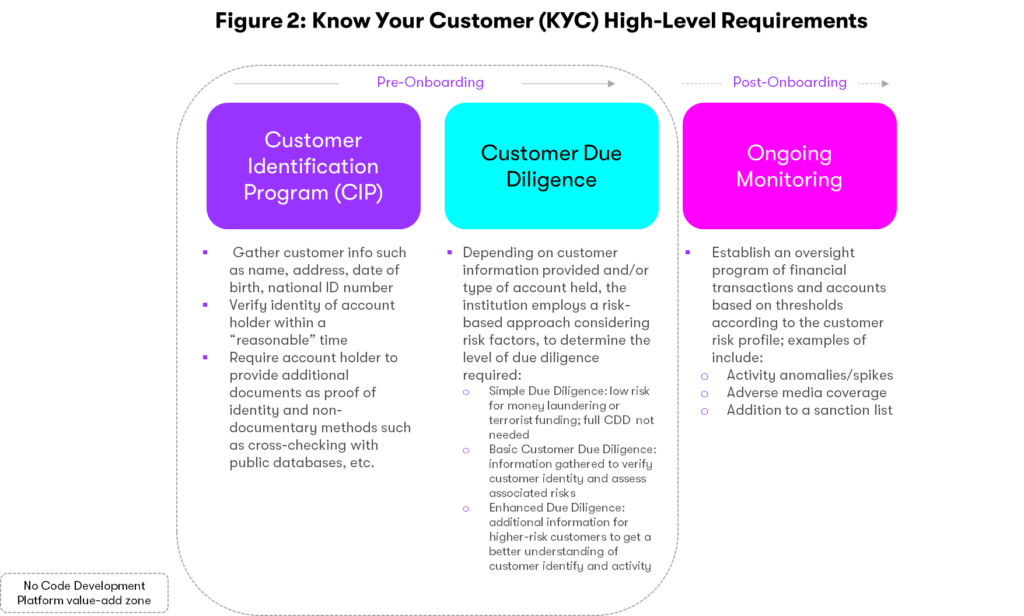

Banks are required by Anti-Money Laundering (AML) laws to implement Know Your Customer (KYC) procedures, an often-onerous process to assess customer risks by ascertaining their identity, financial activities, and overall risk posed – before they can onboard customers. The fines for non-compliance are hefty and real: Kroll, a risk consultancy, found that authorities around the world levied $1bn of AML fines in the first six months of 2021 alone.

Banks are also required to conduct Customer Due Diligence to protect themselves from Politically Exposed Persons (PEPs), criminals, and terrorists. Tedious the first time, continuous monitoring of transactions is required even after a customer is onboarded to flag any suspicious activity or adverse media coverage that they may generate. (See Figure 2)

How NCDPs take the pain out of the account opening & customer onboarding processes

NCDPs enable digitization of account opening forms and workflows to minimize manual data inputs while performing KYC and Customer Due Diligence. Digitizing end-to-end, from obtaining data and documents to digitally signing the application, vastly improves the customer experience and account opening time. And with a robust platform, there’s no need to sacrifice the stringent quality requirements outlined by regulators across the world.

Managing variations in country-specific requirements is simplified with NCDPs like Coherent Spark that flexibly combine data from external databases and user input to provide a holistic profile of the customer that strengthens the customer due diligence process. This digitization unlocks the potential for a truly frictionless customer experience, from start to finish.

Consumer banks widely use Excel spreadsheets with nested credit models. Most would prefer to migrate the models, but the alternatives are not flexible enough or have steep learning curves. This is a significant opportunity for NCDPs to solve one of the industry’s major pain points. For instance, Coherent Spark transforms spreadsheets into APIs within milliseconds. By supercharging their credit models, banks could generate a real-time database to automate their credit assessment and decisioning processes. These APIs can then be exposed to front-end product illustration tools to facilitate the sales process.

Manual credit assessments for cards, personal loans, or mortgages may take days to complete and require reams of documentation. With the help of the automated real-time database, the process can be condensed to minutes, with on-demand data queries from a connected platform. This creates a dynamic feedback loop between the front and middle office, yielding a positive, engaging customer experience with greater transparency and vastly improved processing times.

From a product development and modification standpoint, NCDPs enable the bank’s business functions to create, update, and launch banking products quickly, reducing time to market (TTM). For example, changes to interest rates reflected in product models are usually housed in Excel spreadsheets. Platforms like Coherent Spark help Product and IT teams work more closely together in Agile iterations. They collaboratively create APIs that can be deployed to the cloud for consumption by other banking systems – such as mobile apps and websites. Rapid TTM can provide competitive edge banks are looking for.

Streamlining Support Functions

Banks must comply with numerous regulations that change regularly. Activities are monitored and approved by different departments, which frequently work from spreadsheets. These activities are manual and repetitive, introducing unnecessary risk of errors. NCDPs like Spark can be used to set up a bank or department-wide quality assurance and monitoring hub, with reporting tools and dashboards. This empowers functions such as Risk and Compliance and Internal Audit to cut out manual spreadsheet work and improve data accuracy to help senior management make better decisions.

Summing it all up

NCDPs like Coherent Spark help complicated and highly regulated enterprises launch cutting-edge digital solutions by alleviating pressure on in-house teams and putting instant APIs at their fingertips. The relevance of no-code solutions throughout all banking processes is broad, from customer acquisition to account opening, credit assessment and decisioning. NCDPs have the power to solve many of the industry’s largest pain points.

Front to back, banks can overcome the regulatory and institutional obstacles to digital customer experiences by empowering those with the best understanding of the issues to design the solutions.

Many challenges faced by financial institutions today can now be remedied through lightning-fast calculations and logic directly configured by citizen developers (See Figure 3). From front to back, banks can overcome the regulatory and institutional obstacles to digital customer experiences by empowering those with the best understanding of the issues to design the solutions.

The Coherent Difference

Coherent Spark is here to help jump-start digital transformation – without “breaking the bank.”

The days of a monolithic, expensive, all-in-one solution are fading, and the emerging ecosystem of interconnected no-code development platforms provides better tools, faster adaptation, and far less concentration of risk.

- Proven no-code approach: Coherent Spark uses the world’s most powerful no-code “language” with a decades-long track record and hundreds of millions of users worldwide: Excel. Start using your existing logic assets on day one.

- Governance built-in: Best-in-class audit and control functions cannot be solved with a tacked-on process, so Coherent Spark is designed from the bottom up with transparency and compliance in mind. Audit logs, versioning, and access profiles are part of the fundamental structure of the platform.

- Access the power of the cloud: Coherent Spark lets you run logic on AWS, Azure, or other cloud providers without worrying about software architecture, compatibility, or deployment. Run thousands of data points in parallel or ensure system redundancy for key processes without overhauling your models.

- Stay Connected: With easy integration into market-leading, modern SaaS platforms, ensure there are no gaps in your solution implementation. Whether Salesforce or Shopify, from data lakes to RPA, Coherent Spark complements and completes the tools you use.

Powerful, Smarter, Connected

To learn more about how Coherent Spark can apply in your company, contact us to schedule a demo and a discussion with our Coherent team.

References:

- https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/banking-operations-for-a-customer-centric-world

- Banks Are Using Low-Code To Reduce Backlog Of IT Projects (forbes.com)

- https://www.gartner.com/en/newsroom/press-releases/2021-06-10-gartner-says-the-majority-of-technology-products-and-services-will-be-built-by-professionals-outside-of-it-by-2024

- https://www.mckinsey.com/industries/financial-services/our-insights/remaking-banking-customer-experience-in-response-to-coronavirus

Want to read it later? Download the eBook below so you can read whenever you want, wherever you want, even without an internet connection.

Isabel Feliciano-Wendleken

Chief of Staff to the Global CEO

Isabel is currently the Chief of Staff to Coherent’s Global CEO. She works alongside the executive team to help develop corporate strategy, manage investor relations, and launch strategic initiatives. Prior to Coherent, Isabel started her career in Wall Street as a strategy consultant and held senior management positions at Deloitte Consulting New York, PwC APAC, and Capco Digital Hong Kong. She has advised Fortune 500 global banking and insurance clients on a range of strategic growth and operational improvement initiatives.

-

This author does not have any more posts.

Charlotte Duijl

Customer Success Program Manager

Charlotte is a Programme Manager at Coherent on the Customer Success team based in Hong Kong. She facilitates delivery by helping to successfully implement Coherent’s solutions to their clients. Prior to Coherent, Charlotte was a strategy Consultant at large global consultancy leading complex transformation projects across the financial services sector. With a results-driven mindset and global experience across the US, Europe & Asia; Charlotte aims to foster strong and long-lasting client relationships and successfully bring Coherent’s value-add solutions to market

-

This author does not have any more posts.

Allan Wong

Head of R&D, Coherent Spark

Allan plays dual roles as the Head of R&D for Spark, Coherent’s proprietary logic and rules engine, and as a senior member of the Actuarial team leading client projects. With an insatiable curiosity and collaborative mindset, Allan is focused on helping Coherent’s product managers find innovative and practical ways to use our ever-evolving technological capability. He believes in insurance and financial services as noble professions, centered in protecting lives and legacies, and is passionate about expanding access to quality products through technology.

-

This author does not have any more posts.