Managing personal finances requires strategies for borrowing, saving, investment and protection against risk. As we move through our lives, our needs will change, so as consumers we need a variety of services from banks, asset managers and insurers. Navigating these services is often a challenge, which is why financial advisors play such a crucial role.

Life insurers protect against adversity on a long-term basis, and so the savings elements of their products are always important. Additionally, when insurance policy returns are linked directly to fund performance, or investment indices, the intersection between insurance and wealth management (let’s call it “Insurance & Wealth”) is even more evident.

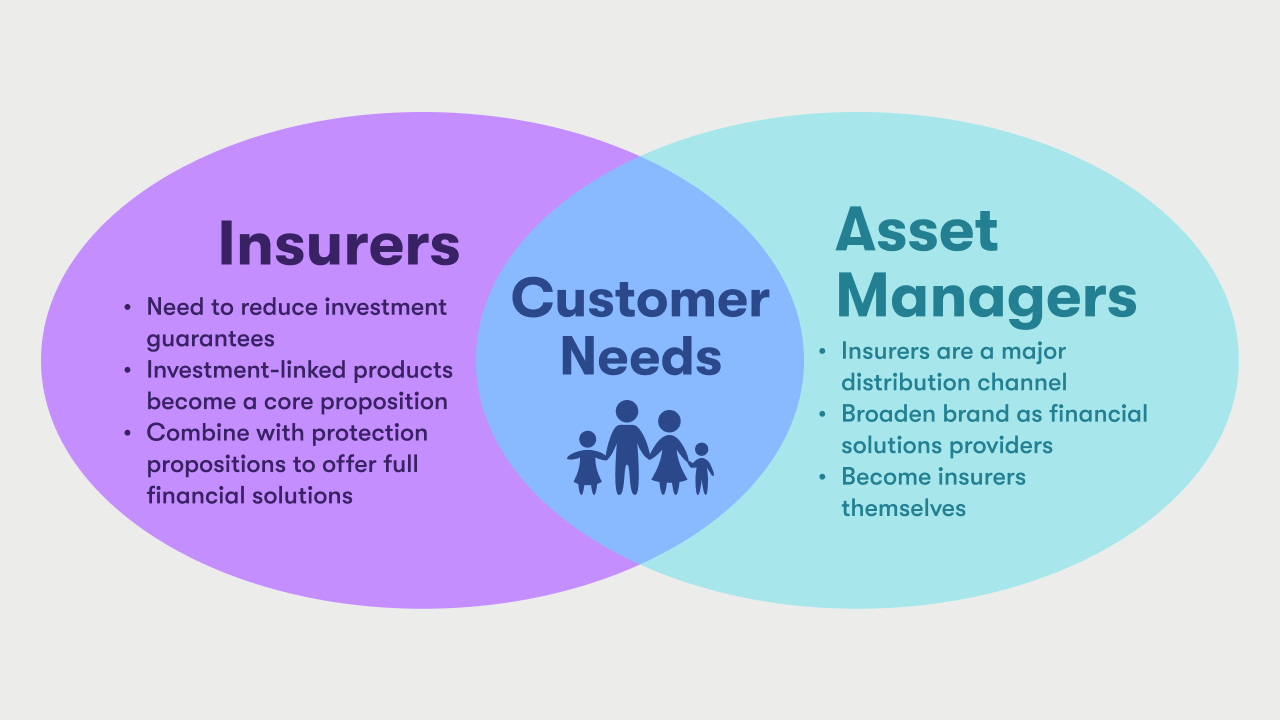

Why does Insurance & Wealth benefit insurers?

Insurers’ sales staff and agents are the primary source of financial advice for many people outside of High-Net-Worth segments. Bundling savings with insurance protection has offered readily accessible wealth management for mass market customers, helping them reach lifestyle aspirations and protect against financial adversity.

Insurance-based savings products typically offer guaranteed returns which suit customers with limited investment experience and a low tolerance for risk. However, in a low-interest rate world, with onerous risk-based capital requirements, significant investment guarantees are unsustainable.

Investment-linked products, for which customer returns follow the underlying asset returns, are more commercially attractive for insurers and offer potentially better long-term outcomes for their customers. So, the confluence of Insurance & Wealth is ripe for growth.

Why does Insurance & Wealth benefit asset managers?

Insurance & Wealth means that asset managers will increasingly work in both competition and partnership with insurers.

Assets underlying investment-linked insurance products are sometimes managed by the insurer’s in-house asset management function, creating more players in the already crowded and competitive asset management industry. So, it’s possible for large insurers with internal investment capabilities to ‘eat the lunch’ of smaller asset managers.

But more often, investment-linked insurance products are a platform on which the funds of multiple asset managers are available to insurance customers. Growth in the market for investment-linked insurance products therefore creates opportunity for asset managers to reach mass market customers who might not buy their funds directly.

What about customers?

Customers don’t care whether financial products are originated by insurers or asset managers. ‘Best-of-breed’ is best for investment savvy buyers, but many customers prefer the convenience of having access to a complete financial solution in one place.

Savings focused customers (savers) like the simplicity and security of bank and deposit products. However, they are very aware that low interest rates supply inadequate returns, or likely negative returns in real terms, even over the long-term. This is the market that insurers have traditionally served with guaranteed return products as savers are wary of the volatility of stock markets and other risk-on assets. Investment-linked insurance products can replace such savings products for inexperienced investors seeking higher long-term returns, but only if they adapt to savers’ lower risk appetites. Investment-linked insurance won’t grow to its full potential if it’s just a means of selling equity funds.

There is a large untapped need for investment products that are relevant to younger customers with newly developing savings habits. This demographic also doesn’t have ready access to financial advice. These customers value:

- Engaging content to explain investment concepts, notably the trade-offs between risk and return.

- Flexibility, for example enabling payments that flex in line with the ups-and-downs of personal budgeting.

- The convenience and on-demand support that comes with a digital-first mentality.

At the other end of the age spectrum, are retirees and pre-retirees. This demographic may be more financially experienced but still needs quality personalized advice. They are targeted with offers for savings products but find it hard to:

- Track total finances across the various bank, wealth management and insurance products that they own.

- Find products that are suited to asset drawdown to meet living costs, as opposed to asset accumulation.

The common theme, across all demographics, is the value of easy-to-understand, personalized, advice. Insurers can provide this at scale through traditional distribution channels, but only via new digital tools to advise and support customers.

Growth of Insurance & Wealth:

Investment-linked insurance is expected to be a major source of growth to 2030.

For example, in Asia, annual Life premiums are currently approximately US$1 trillion1 and growing at 5% per annum. Investment-linked premiums are only 8.4% of this total1, but across markets and insurers we see strategies aiming to increase this share significantly. Our projection is for investment-linked insurance to increase to 25% of total premiums within this decade. With a projected US$1.5 trillion of annual Life premiums by 2030, investment-linked would grow to US$400bn. This means 20% per annum growth in investment-linked insurance to 2030.2

Outside of Asia, we also expect investment-linked growth to exceed overall insurance market growth. In developed markets, mass market retail customers have greater access to third-party advisers which may reduce the proportion of investment products bought from insurers. Yet in a higher inflation environment, real returns on guaranteed savings products will likely further reduce, providing a new tailwind for investment-linked insurance market growth.

Government initiatives to promote retirement saving and investment also promote growth. For example, Hong Kong’s Protection Linked Plan products (expected late 2022) has focused insurers on improving the competitiveness of their investment-linked products.

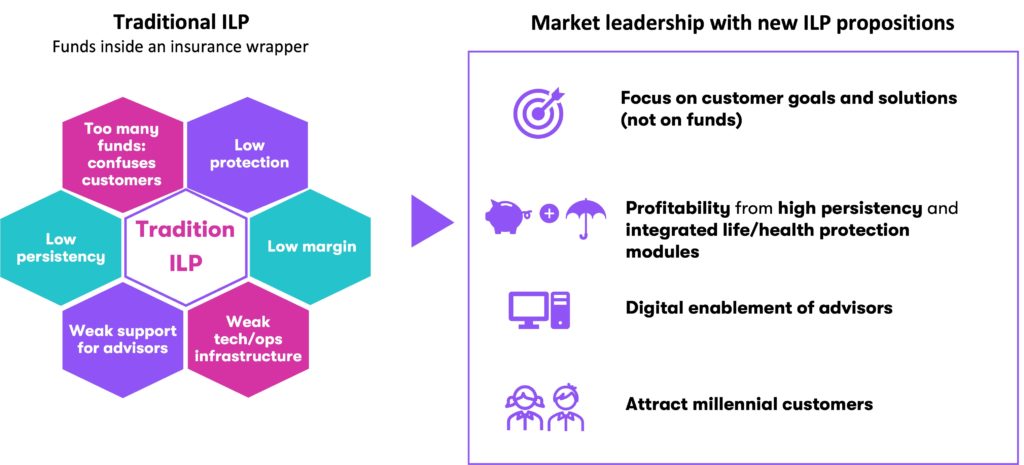

Investment-linked insurance needs to change

For investment-linked insurance to grow to its full potential, insurers will need to differentiate their products from mutual funds and other pure investment products. Additionally, investment-linked products can have a negative reputation. Problem features have been:

- Complexity, especially when there is a plethora of fund options which creates excessive choice for both advisers and customers.

- High charges, with insurer asset charges doubling up on charges of the underlying mutual funds.

- Limited protection coverage, so that higher costs make buying the underlying funds a better customer choice.

- Limited ability to vary premium payments.

- Low persistency, with charges and costs of add-on cover (‘riders’) eroding policy values.

- Poor customer support in respect of fund performance information and policy options.

- Overall, a low level of customer understanding of their policies.

The challenge for insurers is to create fresh savings and protection propositions. To offer combined protection and investment solutions that are straightforward for customers to understand.

This challenge is especially pertinent in markets in which insurers have a large share of mass market savings via participating (‘par’) products. Par-products combine investment guarantees with a share of upside returns distributed as bonuses. As the investment guarantees of par-products become more expensive for insurers, switching to investment-linked insurance makes natural sense.

In several Asian markets, insurers are natural savings product providers because of the strength of their brands and distribution networks. These competitive advantages will only be kept if investment-linked insurance products can meet the needs of an increasingly demanding customer base. We have seen in Europe and Australia that insurers have not always been best placed to offer holistic financial solutions for the mass market; even though that is what many customers need.

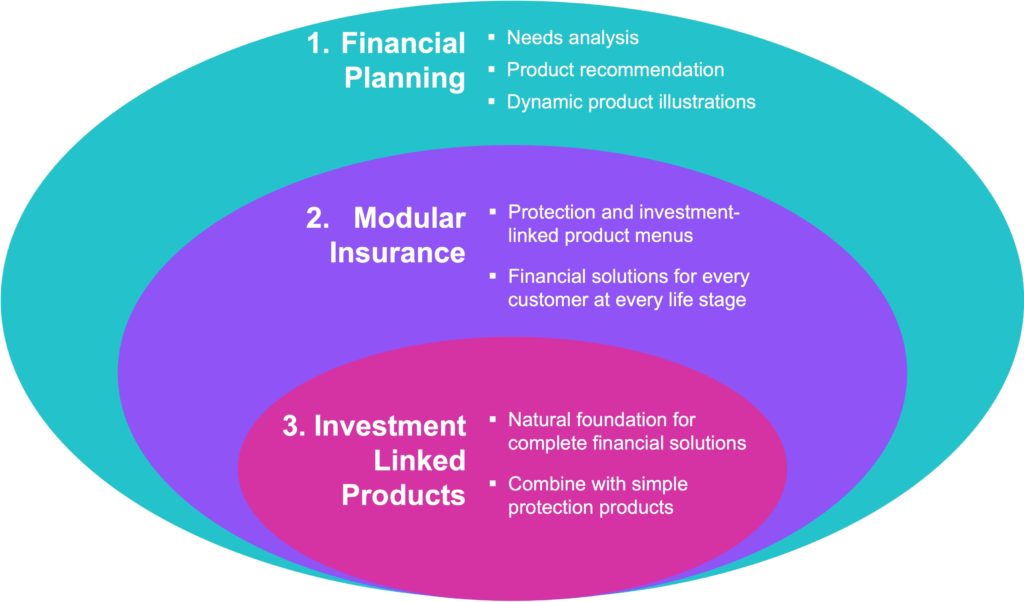

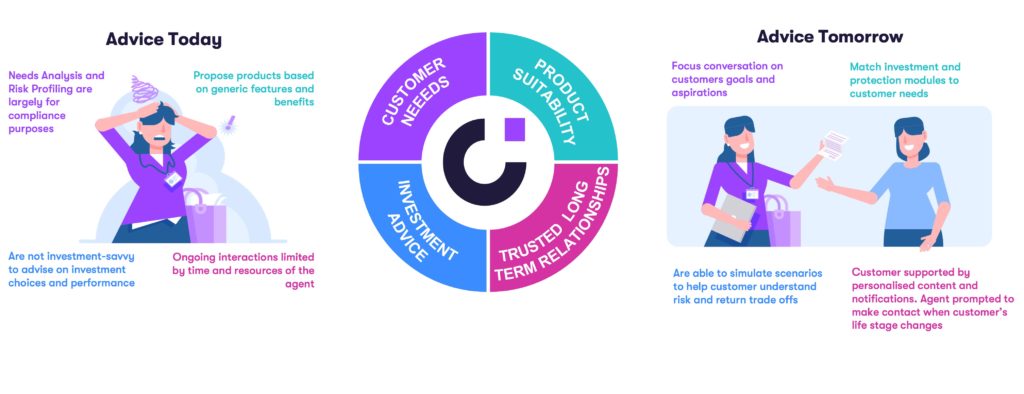

What’s needed: Holistic financial solutions

For Insurance & Wealth to be of benefit to customers, providers need to offer:

- Support to customers to clarify their key life goals and life risks.

- Products that are flexible enough to match:

- The varying needs of different customers.

- The changing needs of individual customers as they move through their lives.

- Support to customers in matching product options to their needs – at point of sale and then on an ongoing basis.

The following diagram illustrates how these apply to providers:

- The proposition of an Insurance & Wealth solution should be much more than product design. Technology, processes, and organizational culture should combine to enable customers understand their current and future needs, and then plan with confidence how these will be met.

- A menu-based, modular, product framework should offer customers both choice and the flexibility to change the choices they make as their needs change.

- The Wealth component of an insurer’s modular framework is most naturally offered by investment-linked insurance modules. These should, with appropriate product charges, offer more flexibility to vary premiums than traditional long-term insurance products.

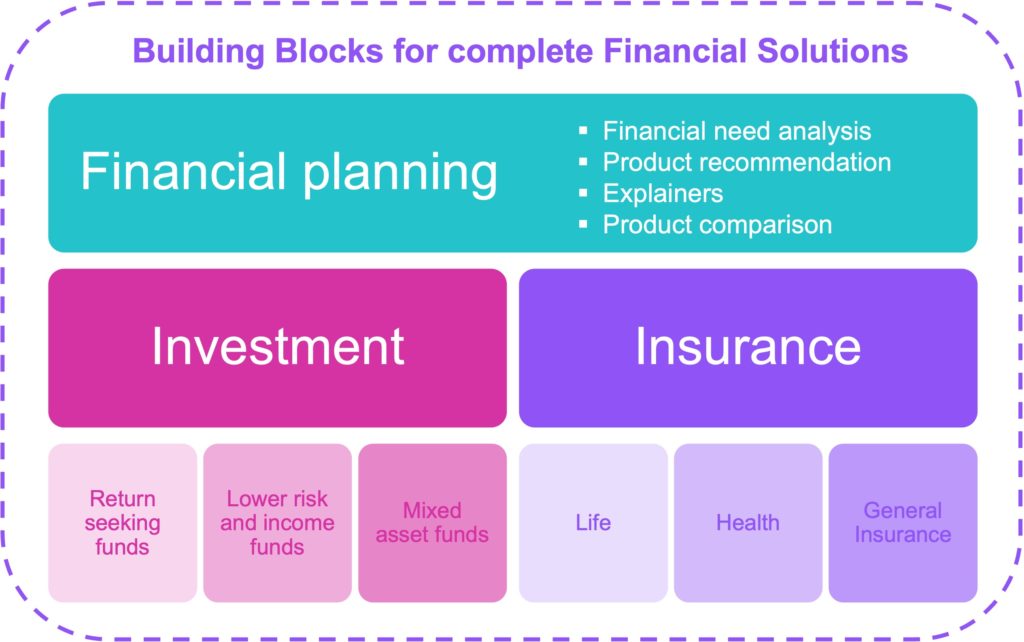

What’s needed: Modular products

The design of a menu-based framework for Insurance & Wealth must strike the right balance between choice and complexity. Too much choice makes the decision-making process overwhelming. Equally, sufficient choices must be offered to meet a full range of customer needs.

From an investment perspective:

A full range of funds across asset classes, investment themes and alternative asset management firms has its place for High-Net-Worth clients who have the means to pay for high quality independent advice; but this is not the situation for most Insurance & Wealth customers.

The priority for savers with little investment experience is to strike the right balance between risk and return for the duration that they expect to invest. A good approach is to offer a small range of mixed-asset portfolios with different risk levels – either as the only option or as an alternative to a range of individual funds for those customers who are comfortable with more choice.

Where investment-linked insurance is offered as an alternative to guaranteed return products, then it is usually the best solution for customers seeking higher returns. However, if investment-linked is the only savings product on offer, then lower risk investment options should be included within the range of investment-linked portfolios on offer.

From a protection perspective:

Investment-linked insurance products typically offer a range of optional protection riders such as top-up life insurance, critical illness, personal accident, and various health coverages. These supplementary coverages provide customers with valuable flexibility and can significantly enhance product profitability for the insurer. This aspect of existing investment-linked products is readily incorporated within a new menu-based framework.

Investment-linked insurance products are written by life insurers and so supplementary protection options are Life and Health coverages. To provide fully holistic solutions there is the opportunity to include General Insurance (Property & Casualty) options, including through a partnership with a General Insurer.

What’s needed: Financial Planning

Customers need support and advice in making financial decisions. However, there are some challenges with this, such as:

- Personalized advice from experienced advisors is expensive, often disproportionately so compared to customers’ premium budgets.

- The economics of third-party advice remunerated by explicit fees, rather than commission, is particularly unrealistic.

- It is considerably more complex to advise holistically on Insurance & Wealth solutions compared to advising on either Insurance or Wealth individually.

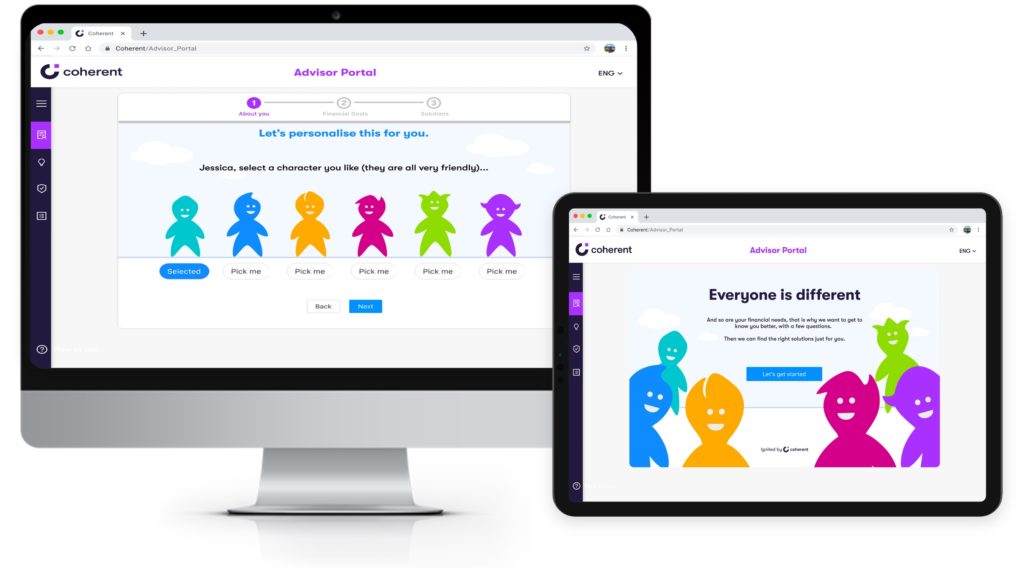

These challenges can only be addressed at scale by technology. Robo-advisors have their place but most customers value advice from a person-to-person discussion. The best use of technology is therefore to equip advisors with digital tools which:

- Prompt customers to supply all relevant information, or access any existing customer data directly.

- Offer a structured approach to identifying customer goals. The advisor can then present these back to the customer for discussion and validation. All ‘solutions’ are meaningless unless the customer’s objectives are clear.

- Set out a proposed solution which can be adjusted in the customer/advisor discussion – often to achieve the right balance between achieving idealized goals and affordability.

Insurance & Wealth Case Study

Coherent worked with an Asian insurer with a new product strategy of evolving its participating business towards holistic Insurance & Wealth. The insurer needed to refocus its agency force accordingly but found the following challenges:

- Agents were well able to articulate the benefits of par-products and were incentivized to offer customers a range of protection riders.

- Agents were uncomfortable proposing investment-linked products because customers always needed help selecting from the extensive range of investment options.

- After-sales support for investment-linked products was much more demanding than with par-products; especially in market downturns when customers became anxious about their reduced policy values.

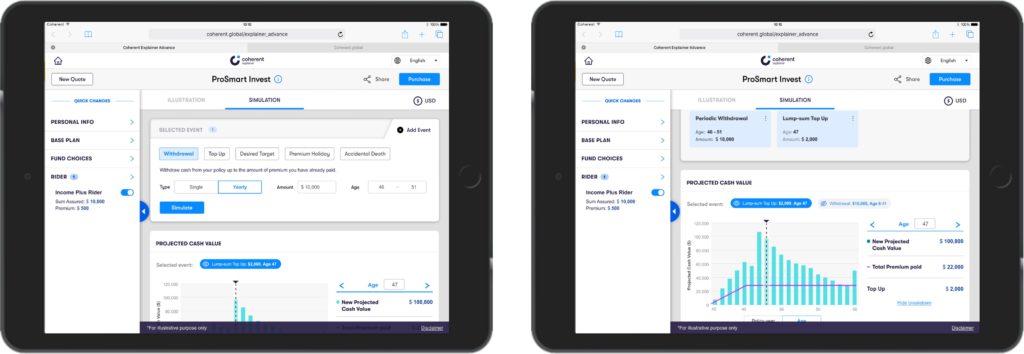

The insurer decided to reorient its investment-linked business from a funds-based to a goals-based approach. This required:

- A digital sales tool enabling agents to support customers set financial goals.

- A set of 10 ‘building block’ funds covering a range of assets classes.

- An algorithm to generate a glidepath of portfolios to maximize the probability of the customer’s goal being achieved.

- An algorithm to propose initial protection coverages and how this could change over time ,including being transparent that lower protection might be appropriate in future as asset values build up.

- A digital customer portal allowing customers to track their progress towards meeting their goals.

- An algorithm to generate notifications to customers should there be a risk of a goal not being achieved.

- Algorithms deployed via Coherent Spark.

By equipping advisors with the tools to steer goal-setting conversations it becomes possible to build an advisory focused salesforce at scale. These conversations must successfully support customers in getting clarity on their financial goals for an automated portfolio construction to add value.

Having put customers into the right product, with suitable fund selections and protection options, it is important to keep customers engaged, including monitoring their investments and changing needs. Traditional distribution channels are not always well placed to support ongoing advice for existing products and so the benefits of investment in digital tools for customers, beyond sales tools, can add significant value in higher retention and higher premiums as customers review their goals.

In this example, the insurer realised that it would frequently need to update the various algorithms; changes in investment markets altered the basis of portfolio recommendation logic and projection of asset values. By deploying these algorithms in Coherent Spark, the underlying models could be immediately adjusted and redeployed without the need for recoding and retesting.

The way forward: Insurance & Wealth

Insurers and asset managers worldwide are reviewing their strategies for Insurance & Wealth. Success means creating investment-linked insurance propositions which offer customers more than funds plus bolt-on protection. Delivering such propositions requires Product, Technology, Operations and Distribution teams to align on new ways of working. Not all will succeed, but the big prize of making financial services more customer relevant is there for the taking.

To learn more about how Coherent’s Spark technology can advance your Insurance & Wealth strategy, contact us to schedule a discussion with our actuarial and technology teams.

References:

- McKinsey: Creating value, finding focus: Global Insurance Report 2022

- Coherent

Bob Charles

Head of Actuarial, Coherent

Bob Charles is an actuary who enjoyed a 30-year career with Willis Towers Watson, culminating in leading the Asia Pacific business. He subsequently worked with insurance technology start-ups. Bob is currently the Head of Actuarial at Coherent, working with clients on finding great uses-cases and applications for our unique Spark technology.

-

This author does not have any more posts.